Fast, flexible finance—without affecting your existing mortgage

Second Charge Bridging

Access the equity in your property without refinancing or disrupting your current deal. Short-term finance structured to move at speed when timing matters.

Second Charge Bridging Loans

A faster way to raise capital—without remortgaging

A second charge bridging loan is a short-term finance facility secured against your property, sitting behind your existing mortgage. Your current lender, rate, and terms remain unchanged. At the same time, you release additional capital based on the equity you’ve built.

It’s a practical way to raise finance quickly—without restructuring your main borrowing or losing a favourable deal.

Why use second charge bridging finance?

Some situations don’t allow for slow processes or standard lending timelines. Remortgaging can work, but it often introduces delays, early repayment charges, or unnecessary change.

- Keep your existing mortgage in place

- Arrange finance within days, not months

- Avoid early repayment charges on your main loan

- Work around real timelines and non-standard situations

- Use it as a short-term solution with a clear exit

Important information

Your home may be repossessed if you do not keep up repayments on your mortgage.

There will be a fee for bridging loan advice. The fee is up to 1% of the loan amount and will be no more than £4995

Who can benefit from Second Charge Bridging Loans?

Homeowners managing a gap between buying and selling

Property investors acting on time-sensitive opportunities

Borrowers with complex income or structures

Anyone needing finance without disrupting an existing mortgage

Borrowers with a defined short-term need

Equity-rich homeowners needing quick access to capital

When timing matters: how is the loan used?

Second charge bridging finance is typically used where access to capital is needed quickly and a longer-term solution is not yet in place.

Common uses include:

- Funding property renovations or refurbishments to increase value ahead of sale or refinance

- Raising a deposit to secure an additional property, including buy-to-let or auction purchases

- Injecting short-term working capital into a business for expansion, stock, or cash flow

- Settling time-sensitive tax liabilities, such as Inheritance Tax, VAT, or Corporation Tax

- Financing a lease extension or freehold purchase to improve a property’s value and mortgageability

- Preventing a property chain break while waiting for an existing sale to complete

- Releasing equity without disturbing an existing first-charge mortgage or incurring early repayment charges

- Consolidating short-term liabilities ahead of a planned refinance or exit it

1st vs 2nd Charge Loans

A second charge bridging loan is secured against a property that already has a mortgage in place. The new lender takes a “second charge,” meaning your existing mortgage remains first in priority.

Before the loan is completed, the first-charge lender is notified, and consent is obtained where required. The second charge lender then provides the additional finance based on the available equity and the agreed exit strategy.

The loan is structured on a short-term basis and repaid once the underlying objective is achieved—typically through sale or refinance.

What types of property can be used as security?

Second charge bridging loans can be secured against a range of property types, subject to lender criteria:

- Residential property – main residence or second home (regulated where applicable)

- Buy-to-let property – rental investments

- Commercial property – offices, retail units, warehouses or industrial space

- Semi-commercial property – mixed-use buildings (e.g. shop with flats above)

- HMOs (Houses in Multiple Occupation) – multi-tenant residential properties

- Land – typically with planning permission in place

- Property portfolios – multiple properties used together to maximise available equity

Who We Work With

We work with leading lenders across the market to match you with the right deal.

Considerations

Exit Strategy: How will you pay it back? Typical loan term is 12 months, so you need to make sure that the exit strategy is solid. Examples: Your property sells, re-mortgage, equity release or inheritance.

Interest Rates: Loan to Value (LTV) affects your interest rates which can be much lower under 55% loan-to-value. Compared to a mortgage – the interest rates are comparatively higher than a traditional mortgage. If less expensive options are available, we will make that clear at the outset. If Bridging is the only option, we work hard to minimise any costs to you and also keep your monthly interest as low as possible.

Think carefully before securing a bridging loan against your property. your property may be repossessed if you do not keep up repayments on a bridging loan, mortgage or any other debt secured on it.

How it Works

Fill Out Our Form

One of our certified advisors will call you

Tell Us About Your Needs

Once we understand your circumstances, we will search our panel to find your best options.

We Will Provide You With Options

When we find the right match, we’ll explain your options clearly.

Loan Application Online

Our secured loan application process in done fully online. We’ll be with you every step, all the way to approval.

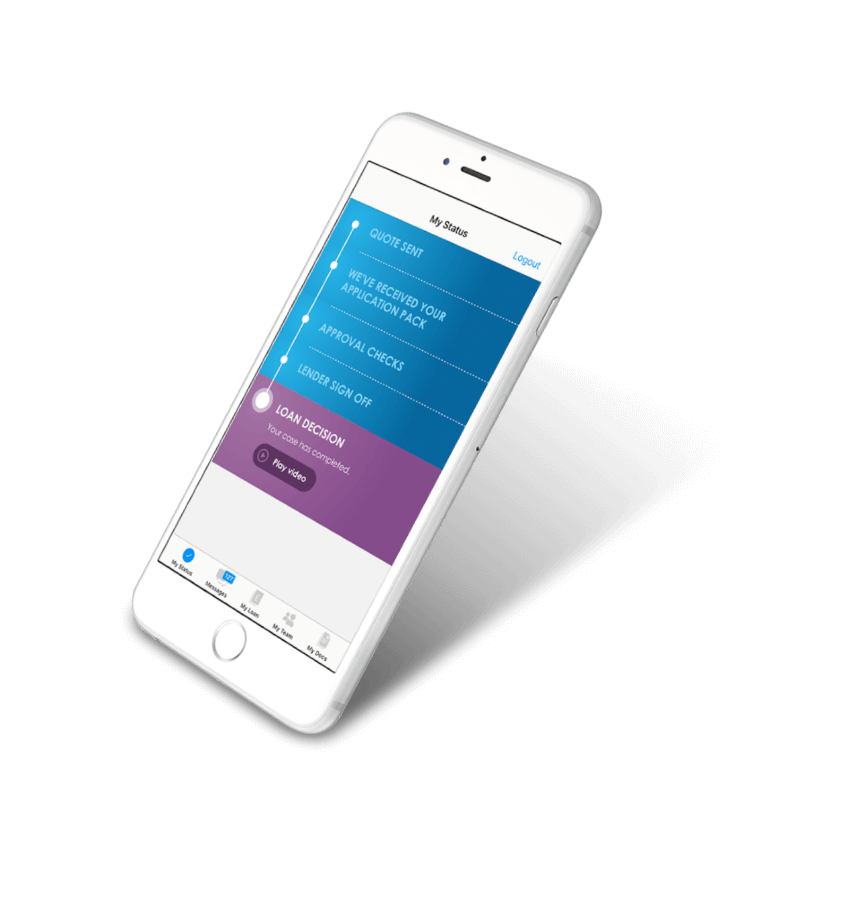

Stay in the Loop 24/7 with MyFluent App

View the progress of the loan application in real time and easily communicate with your dedicated Case Manager.

Why People Choose Fluent Money

Low Interest Rates

Rates for second charge loans against property can be lower because there’s less risk for lenders, with your home as security.

Borrow Larger Sums of Money

Lenders are often more willing to lend larger sums (£10,000 – £500,000) because your property secures the loan.

Lower Monthly Repayments

Most second charge loans can be repaid over the long term (3 to 30 years). This often means lower monthly repayments, making them more manageable. But remember: spreading payments out can increase the total cost.

Panel of Leading Second Charge Lenders

It allows us to provide you with options tailored to your needs.

FAQs

No. A second charge bridging loan sits behind your existing mortgage. Your current lender and terms remain unchanged.

Timeframes vary depending on the details of the case, but second charge bridging loans are structured to move significantly faster than traditional lending where all information is available. Therefore, often within a few days.

No. Cases are assessed individually, with more flexibility than many mainstream lending options.

Repayment is typically based on a clear exit strategy, such as the sale of a property or refinancing onto a longer-term product

Move forward with the right structure in place

If you need to raise capital quickly without disrupting your existing mortgage, a second charge bridging loan offers a direct and workable route.

Why Our Customers Recommend Fluent Money®

We’re one of the UK’s favourite finance brokers. Don’t believe us? See what our customers have to say:

Amazing

First time using the service for a bridging loan as our house sale completion was effectively taking longer than expected and had to break the chain to ensure we were able to complete house purchase. Matt was really helpful in explaining options, costs and finding the option that tailored to our needs. Gemma then helped through the steps to completion – all in all took a week to complete the whole process. Fantastic service.

Excellent Start to Finish

Once I had decided to accept the Bridging loan, I downloaded the app and it was very easy to use and the messaging service was the most efficient way I have ever had the pleasure to communicate via. From the initial enquiry, I was informed every step of the way. Every query was answered immediately via the instant message on the app (very impressive). Thank you to Gemma and her team.

What an amazing company!

We needed a bridging loan and chose Fluent Money. The whole process was seamless. I can’t recommend them highly enough!

Great service from first enquiry to completion

This is the first time we’d needed a bridging loan, but Fluent led us through the process. They were friendly yet very professional, from Ellie who answered my first query, through Matt, to Jessica, who was so supportive right through to the end. Nothing seemed to phase her. She always answered really quickly, and settled our wobbles. We weren’t prepared for some of the weirder questions from the lending bank’s solicitors, but that wasn’t the fault of Fluent! Jessica always managed to calm us!

Bridging Finance Success

Fluent successfully placed my bridging finance application, on standard terms, after four previous rejections with other brokers. Broker fee was relatively high but not due until after completion. My Adviser and Case Manager were both very helpful and efficient.